Effects of Russia’s war on European coal phase-out

By Lola Nacke & Jessica Jewell

As the EU wrestles over the timeline of its embargo on Russian coal, a larger question looms over the future of coal in Europe. Prior to the war, most EU countries had pledged to phase-out coal by 2030 and the remaining had plans in the works for phasing out coal by 2049 at the latest. Does the war in Ukraine and concerns over natural gas risk delaying these plans? Here we investigate this question by examining the energy security situation in different countries as well as statements EU countries have made about their coal phase-out plans.

Why is coal phase-out at risk of being delayed?

Europe imports coal, gas and oil from Russia and has pledged to stop importing all fossil fuels well before 2030. The most difficult of these to stop importing is natural gas due to the high dependence on Russia through pipelines combined with reliance on the fuel in heating and power generation. As we discuss in an earlier post, Europe imports about the same amount of natural gas from Russia as it uses in electricity generation. That may place Europe’s coal phase-out plans in jeopardy since arguably the most readily available substitute for gas in power generation is coal, because existing infrastructure can be used by substituting the fuel, whereas increasing renewables capacity will require time to build.

Where is coal phase-out at risk of being delayed?

This means that among all European countries with coal phase-out commitments, those most at risk for delaying coal phase-out would be those with the most Russian gas in their energy mix and the most domestic coal resources.

While rising natural gas prices can affect all countries which use gas, the most immediate threat to energy security comes from those with a high reliance on Russian gas due to the risk it poses to energy security and the financial flows it ensures for Russia. Out of all European countries that have announced coal phase-out commitments, the Netherlands has the highest share of gas in their energy mix at 45%, about one third of which it imports from Russia (Figure 1). Countries like Slovakia, Czechia and North Macedonia use less gas overall but import 100% of their natural gas from Russia, while Germany, Italy and Poland import about 50%.

Figure 1: Share of Russian and non-Russian gas in national energy mix in EU countries with coal phase-out plans. All data for 2019. Source: Own calculations based on IEA Energy Balances (Share of gas in TPES) and Eurostat (Proportion of gas imported from Russia).

At the same time, some of these countries have a high amount of domestic coal in their electricity mix (Figure 2). Poland generates about 60% of its electricity from domestic coal and Czechia almost 50%. Countries with a large supply of domestic coal could be most at risk of delaying phase-out because using a domestic resource promises higher overall import independence, which is likely an important goal in times of political instability. Additionally, delaying coal phase-out may be in line with current national political discourses and strategies to appease politically influential coal mining companies and unions.

Figure 2: Share of domestic coal, imported non-Russian coal, and Russian coal in national electricity generation in EU countries with coal phase-out. All data for 2019. Source: Own calculations based on IEA Energy Balances (Share of coal in electricity and share of total imported coal) and Eurostat (Share of coal imported from Russia).

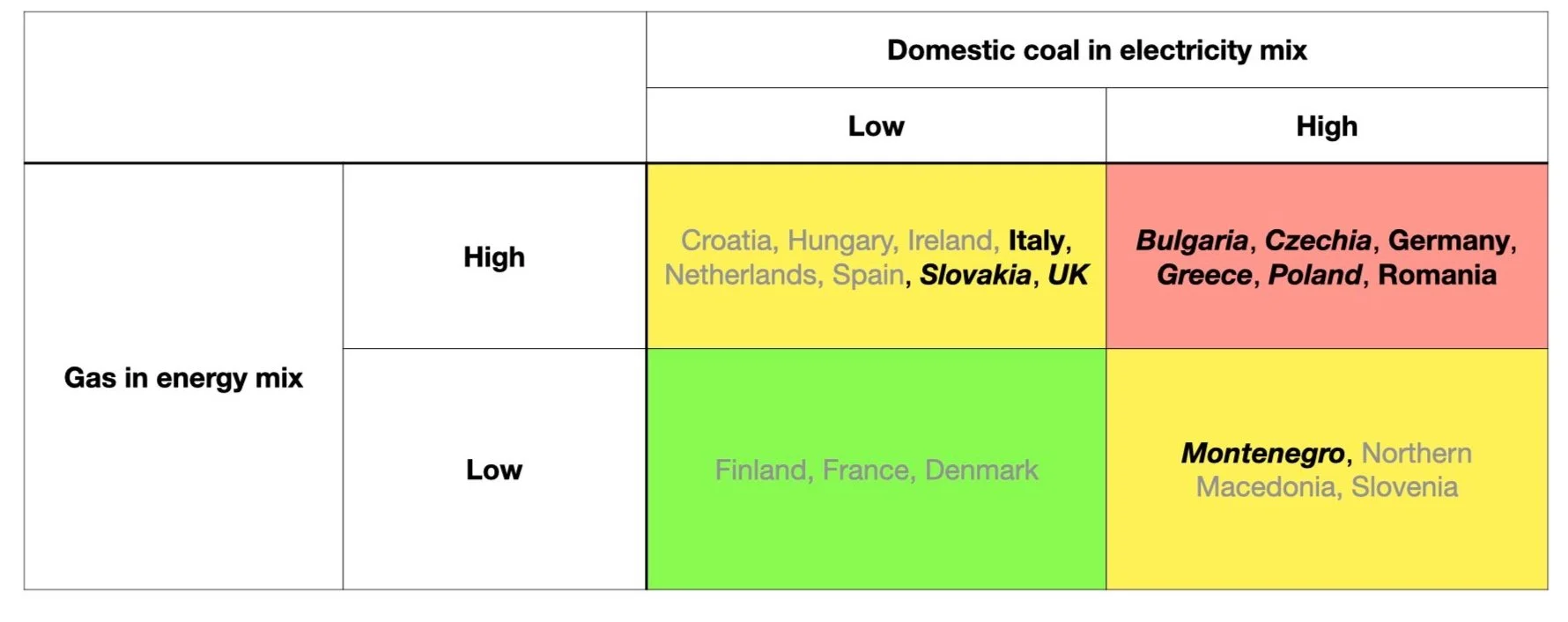

Below, we compile a matrix for which European countries with coal phase-out commitments may be most at risk of delaying coal phase-out. Countries with a high share of domestic coal (larger than 10%) and high share of gas (higher than 15% or at least 10% Russian gas) in their electricity mix are categorised as being at high risk, and marked in red. Countries with a low share of gas in their energy mix and a low supply of domestic coal in electricity (<10%) are marked in green and are considered to be at lower risk of delaying their phase-out commitments. Countries marked in yellow, with either low supply of domestic coal and high share of gas, or vice versa, are considered at being at moderate risk of delaying their phase-out commitments.

Table 1: Risk assessment of coal phase-out delay for European countries based on share of gas in national energy mix and share of domestic coal in national electricity mix. Countries marked in bold have indicated likely phase-out delay. Countries marked in italics, have had discussions of a potential coal phase-out delay.

In fact, governments from several countries have released statements signaling an increased use of domestic coal at least in the short-term, and some even point at the potential of delaying coal phase-out all together. For example, Czechia’s energy security commissioner, stated that “There is a temporary role for coal, which we had hoped would be out of the energy mix by the end of this decade. But it will stay longer.” Poland’s Economy Minister called for a “reactivation of coal extraction in Poland”" and the country has plans to become independent from Russian gas by the end of 2022. Furthermore, Germany is now considering keeping coal plants in reserve, and Bulgaria “is ready to keep its coal industry till the construction of a minimum of two new nuclear reactors”.

These signs show that over the short-term, coal phase-out is likely to experience a delay in several countries due to the new geopolitical system. However, the big question is what will happen to coal in the long-term. Will these new energy security concerns lead to a significant delay in Europe’s coal phase-out? Or will concerns accelerate the deployment of low-carbon alternatives and the demise of coal?

Methods note

To show which countries use most gas in their energy supply and have most domestic coal in their electricity mix we use data for 2019 because electricity supply and demand (including coal generation) dipped in 2020 due to COVID restrictions. The electricity use (and coal generation) in most countries has bounced back since the 2020 dip. As a result, we believe 2019 is a better analogue for the current situation than 2020.

This entry was also published on the Coal Transitions platform as part of the CINTRAN project.